Some thoughts on precious metals

20240828

I’ve been hacking away at this piece for a week. I have not yet integrated it into my Bartercoin piece, and may not get around to it.

In addition to reading voraciously, I have been watching quite a bit of video. One has to – the better minds are not reducing as much to print any more. Though confirmation bias is social media’s modus operandi, there is absolutely no author with whom I agree completely.

I project – I know – that none of you out there agree with me entirely. I’m content to be who I am, and that I don’t have to make money by writing things that will have youu nodding your heads in rhythm. At this point I’m thinking of putting out short, disconnected pieces about the various thinkers I have read. Meanwhile, this on precious metals and Bartercoin. Thanks to streamfortyseven for his many comments. He has read very widely on many topics. While I don’t always agree, he is invariably worth listening to.

Graham

Gold is not overpriced

When I wrote my Bartercoin piece in April gold was at about $2370. It is now $2515, or an annual rate of 12%. Nothing unusual. I recently that Silvercrest CEO Chris Richie found in his survey of 400 assets he might keep on his balance sheet that they average 6% annual appreciation since 1990. From $35 to $2500 amounts to about 6% annually since the 1950s for gold. For what it is worth, Washington D.C. real estate has also appreciated about 6% per year since the 1970s.

Although gold is at an all-time high relative to the dollar, it is well below its inflation-adjusted highs of 2011. I offer two contradictory notes. First, all world governments, led by the United States, have had covert, sometimes overtly expressed policies of suppressing the price of gold since the time of Roosevelt. They want money to be invested in other things such as the stock market and housing, and they want people to hold fiat currency instead of metals as investments. Second, somewhat contradictorily, gold mining companies have been able to operate profitably throughout this period. Supply has balanced demand.

History tells me that gold is not overpriced. If the price suppression mechanisms the Gold Anti-Trust Action Committee documents were abandoned the price would probably rise. But the biggest impetus for a rise is likely to come from inflation. Central banks have had to borrow to balance national budgets all over the world. The debt-to-GDP ratio is now well over the 103% at the end of World War II.

Inflation will accelerate

Inflation in a time of all-out war is to be expected. WWII’s end brought that ratio down to about 30% in the Nixon/Ford years. Now, however, even in peacetime the US government spends $4 for every $3 in tax revenue. They cannot raise taxes. They have no choice but to print money to paper over the deficit.

All world governments are doing essentially the same. This has happened over and over throughout history, every time ending in a financial collapse. The wrinkles are different this time. The crisis has never before been absolutely world-wide, the central banks have never worked so diligently in such a coordinated fashion to kick the can down the road, and there was always previously enough population expansion to grow out of it. Never before have the most productive populations – of European and Northeast Asian descent – seen such massive collapses in their birthrates.

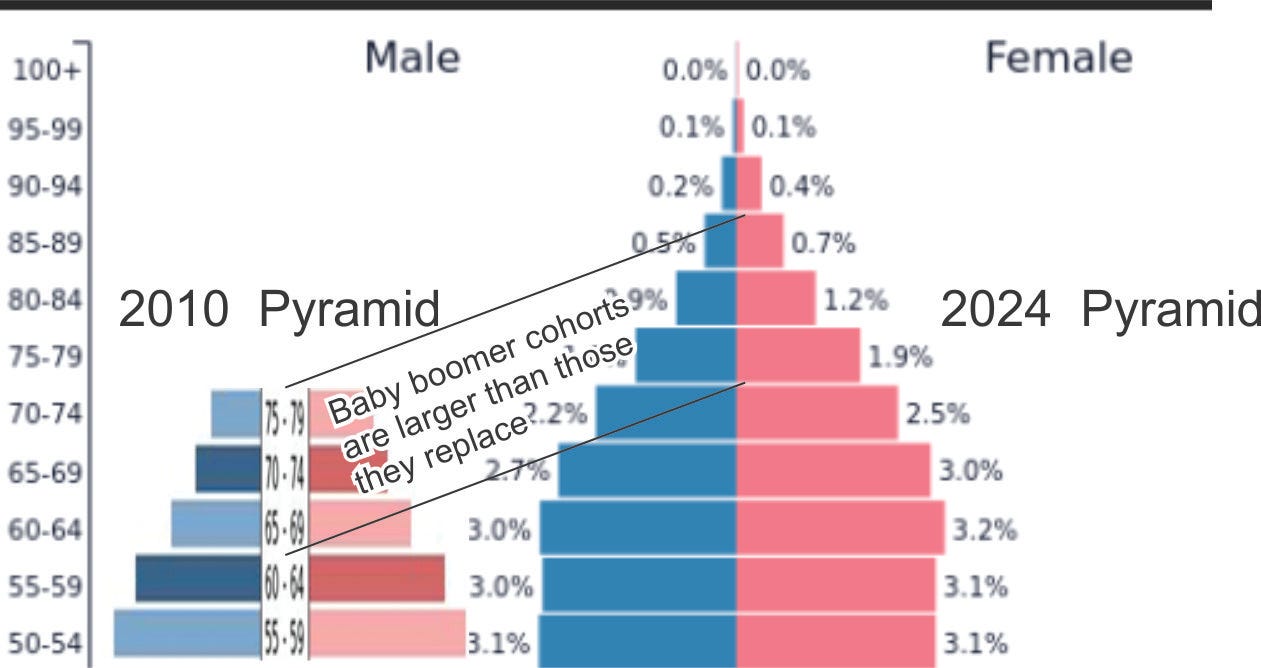

The result of having fewer productive people to tax and more who depend on government for their income must be a decrease in relative income. Governments are loath to cut social benefits directly. Their only viable option is to minimize annual increases and let inflation cut their real value – as has been happening for years with Social Security in the United States. The downward spiral can only accelerate as the large Boomer generation continues to retire.

This diagram shows that the Baby Boom cohorts that have entered, and will enter, retirement are far larger than those they replace. Among those below retirement age, Gen Xers, the cohorts are about the same size. There are fewer and fewer workers to support more and more retirees.

The world's current demographic situation is without precedent. The United States demographic pyramid is turned into a demographic spindle, each succeeding generation smaller in size, even despite immigration. The native-born American population of European and North Asian extraction is absolutely refusing to procreate, as in Northeast Asia itself and in Europe. What fertility there remains in those countries is among people who are unlike them. They differ in their ethical makeup, their temperament, and sadly, usually their intelligence. The intelligent populations of the world are not reproducing themselves. From the top down these are Jews, Northeast Asians and Europeans.

Comparing major classes of investments going forward

The major classes of investments have customarily been broken down into real estate, productive assets such as enterprise ownership via small business ownership and shareholding, and holdings of non-productive assets such as commodities, precious metals and currencies. Conventional wisdom has long favored the first two. Human ingenuity has led us to create more attractive products and services such as computers, communications, and leisure time goods. A growing population favored real estate – land is a scarce commodity, and growing populations meant increasing demand. Commodities, on the other hand, just sit there. They don’t grow, and preserving and protecting them takes resources.

The arithmetic is changing. As populations stabilize and shrink there is more than enough acreage for everybody. Exuberant democratic spirit has empowered populations of less capable people. The relaxation of Darwinian pressure has allowed their numbers to grow. They predominate in urban areas worldwide, making city living less attractive. Many big American cities are long past the tipping point. People do not want to own houses in Detroit, Baltimore or St. Louis. San Francisco, Portland, Seattle and many others are at the tipping point. Capable people are abandoning them in droves.

Real Estate

The upshot is that urban real estate is a decreasingly attractive investment. Exurban land remains too plentiful to see much inflation. The stable to decreasing population of people doing office work can and do work remotely. Commercial real estate likewise. Offices are standing empty; mall shopping is dangerous and Internet shopping easier. Real estate is a sitting duck for the ever more voracious tax man.

A little arithmetic should convince anybody that there is land enough for everybody in the country, even including illegal immigrants, to own houses. A quick glance at Nicaragua, Ukraine or any African country should be enough to convince you that adequate shelter need not cost a million dollars. Removing inessential zoning, building codes, property taxes and other such impediments it is possible to build and inhabit a livable house for little more than an average annual salary. Habitat for Humanity proves it over and over again.

What is missing is the skill and enterprise to build your own house. There are many houses under construction by owners in my Kyiv neighborhood. I doubt you see it where you are. The upside of increased specialization is higher average income. The downside is a complex society in which individuals are more total dependent on one another.

One should conclude that the perceived housing shortage is an artificial creation of governments, bankers and corporate interests. If the situation can be so remedied, real estate is not as scarce as it appears and is hence not a great long-term investment. Burnishing my concept of myself as being ahead of the curve, here is QTR guest Harris Kupperman writing about just such a megatrend. He mentions JOE – that’s St. Joe, a Florida land company. Same idea, different geography.

Public companies

If not real estate, how about stock ownership? Publicly owned companies of the 19th century satisfied basic needs such as rail transport, steel, electricity and petroleum. Those of the 20th century continued satisfying basic needs with automobiles, airplanes and telephones, and verged over into satisfying universal desires – air conditioning, home appliances, entertainment and communications.

The publicly owned behemoths of the present age make you, the consumer, their major product. Google, Facebook, Microsoft and Amazon monetize what they know about you. Apple and Nvidia’s products make it possible to captivate you. Tesla sells at a sky-high multiple precisely because it is designed to flatter human desires rather than satisfy any basic human need beyond that which Henry Ford addressed. The largest advertisers, pharmaceutical companies, impart the impossible dream of perfect health and a carefree life and offer chemical compounds to supposedly satisfy the dream. Their products make you dependent and subtly (or not) create additional problems for which they happen to offer chemical solutions.

Though it may not so appear at the present, these companies that satisfy artificially created wants and needs may not hold up so well in an economic downturn. They are all deeply entwined with the US government and banks, which appear to have used market manipulations to artificially inflate capitalizations, especially of these “magnificent seven” that drive market indices. In doing so they (1) reward the political allies of the deep state, (2) create the illusion of a prosperous society, (3) artificially inflate the reported value of pension fund holdings and hence the illusion that there can be a prosperous retirement, (4) make investing in companies which produce little more than vapor more attractive than investing in hard assets.

This long-sustained euphoria appears to be ending. When it does, there is likely to be a newfound appreciation for companies and people that satisfy basic human needs such as food, water, shelter, energy, public safety, health and transportation. There will be an appreciation for real estate simply as shelter, an abundance, not an investable scarcity. All a person really needs is a roof over his family’s head.

Commodities

Commodities are attractive in times of uncertainty. Preppers are right to say that a family should have a stock of non-perishable groceries, automotive fuel and perhaps warmth in the form of a woodpile. There are practical limits, however, in that they take up space and must be preserved and safeguarded.

Precious metals are the exception, a compact and non-perishable form of storing wealth. One house is enough for one family. You can’t take it with you if you are forced to flee, and you can’t dodge real estate taxes. On the other hand, a person can never own too much gold. Each additional coin represents another few months’ food in a time of crisis. Put another way, the market for gold will never be saturated in the way a real estate, cocoa or iPhone market can be. People can always use more. To look at gold in yet a third way, for each of the world’s eight billion people there has been only one ounce of gold ever mined. The vast majority have none at all. The world’s thirst for precious metals will not be soon slaked.

Cash

A person should always have cash on hand. When it was backed by gold and there was little inflation, holding quite a bit made sense. Now, with fiat currencies losing 5% or more of their value per year, depending on whose claims you believe, cash is no longer as attractive. With the advent of central bank digital currencies, in which your financial life becomes an open book, it is even less attractive.

Central bank digital currencies will change the situation

Digital currencies are a threat to privacy and hence to personal freedom. They will be a powerful tool with which government can impose its will over the citizenry. It behooves us to understand their implications and mechanisms to avoid being forced to use them.

Characteristics of a monetary transaction

Money is involved in financial exchanges, that is, every exchange of value except barter. There are several characteristics of a financial transaction.

The transaction may or may not be recorded in some searchable fashion.

The transaction may be direct or employ financial intermediaries

The parties may be face-to-face or remote

Parties may or may not be identified to one another

Parties may or may not trust each other.

The transaction may be reversible or not.

The transaction may be legal or illegal.

Assuming a transaction is recorded and traceable, it will be visible to law enforcement and tax authorities. It matters only in degree whether the visibility is through a credit or debit card, a central bank digital currency, cryptocurrency or digital communications. Some media make tracing harder than others, but they all permit it. Anonymity requires unrecorded and untraceable transactions. We can be confident that politicians will want them for receiving a bribe or paying their mistresses. Anonymity, freedom from scrutiny, also serves us hoi polloi.

We know the problems of questionable transactions being conducted via financial intermediaries such as banks. When Eliot Spitzer paid a prostitute through financial institutions, albeit via a series of cutouts, prosecutors were still able to put the dots together and drive him from office. Michael Cohen caused endless grief for Donald Trump by paying off Stormy Daniels in a traceable transaction – one that Trump says he didn’t authorize, for a skanky commodity that he never would have wanted and certainly, per Billy Bush, would not have needed to pay for. The Bitcoin companies Pirate Bay and Silk Road found that the anonymity provided by Bitcoin was not enough to protect them. Forensic sleuths were able to piece together enough of the story to search for corroborating evidence to convict them.

There are some transactions that are traceable but for which excuses can be concocted. Hunter Biden sold paintings for extraordinary sums of money. Hillary Clinton gives speeches for similar sums of money. Nelson Rockefeller paid his mistress for research services. Willie Brown of California, paid his mistress, Kamala Harris by promoting her career. These transactions may be transparent bribes, but they at least have an alibi to defend them. Anonymity would play no role in transactions such as these which do have a questionable quid pro quo, but are nonetheless traceable.

Precious metals – untraceable transactions

Precious metals would serve the kind of transaction that a participant would not want traced, such as a politician, having a call girl come to his room, or a City Councilman taking a payment for influencing a procurement decision. Or, more likely, an ordinary citizen like you or me purchasing a firearm that we do not want the government to confiscate, a husband buying a birthday present that he wants to keep as a surprise, or going to a doctor to for diagnosis of a possible sexually-transmitted disease.

These are perfectly legal and not totally dishonorable things, but you want to suppress the information. How do you do it?

Problems with paper money

Currently, such transactions would usually be handled in cash. US dollars are used throughout the world for the sort of thing. Politicians in every country are prone to have stashes of US dollars hidden in safes behind pictures on the wall and under floorboards.

What will happen when and if US dollars paper US dollars must be turned in, in exchange for central bank digital currency?

This is not a hypothetical situation. During the conversion to the euro, for instance, millions of dollars’ worth of Deutschmarks, French francs, Italian lira and such needed to be exchanged for the new currency. It caused some embarrassment to the holders of illicitly acquired cash.

Similar situations arose in wartime. The US military in Vietnam issued MPC's, military payment certificates, denominated in US dollars. They periodically changed the issue of the MPC, requiring that people convert the old to new. If holders didn't have a good explanation where they got the old, they lost it.

After the fall of the Soviet Union the ruble lost its value. The banks were frozen. People who had Soviet rubles in the bank could not exchange them. They suffered a haircut of 70 or 80% when the banks reopened and exchangeability was restored.

In looking for alternatives for cash transactions, one could hope that there would remain paper currencies still in circulation in the world to facilitate anonymous transactions. They may be Saudi Arabian rials, Thai baht, or perhaps a BRICS currency. We can expect that such currencies will enjoy greater circulation by virtue of their anonymity. They would will work as immediate means of exchange if they are widely held, easily available, and not subject to violent inflation.

Using currencies requires either a face-to-face transaction in which the quid pro quo is exchanged in real time, or a matter of trust. If you mail anonymous currency to somebody, you have to trust that you get what you paid for. If there is no trusted intermediary, the transaction may not be possible.

When people are dealing in other than their native currency, there is always an exchange-rate question. You would have to know the exchange rate between the transaction medium and the price, probably quoted in the national currency. There has to be a trusted exchange-rate known to all parties. Most exchange rates such as currencies and precious metals are published daily on the Internet.

There has to be has to be a means of verification. Especially if you are dealing with currency bills with paper currency not in your own currency. How do you know the bills are authentic? For small transactions you can take a risk, for larger ones you cannot. How can you tell if the notes are counterfeit? For instance, if you are buying a car in Poland with Saudi with Saudi rials, how can the seller know that your Saudi rials are real? How can you know where the car came from? Are a lot of unknowns.

It boils down to a question of creating a currency that is that can be immediately validated but is nonetheless anonymous. The money that has withstood the test of time is precious metals. Precious metals have intrinsic value. If you can verify that a coin is made of pure metal, and weigh it or trust by eyeball the minted denomination, or trust a certificate that accompanies it, you can accept it at face value. The Bartercoin system is going to answer the question of how you do this.

An aside here. If you are dealing with banknotes, the anonymity is compromised by the serial numbers on the currency. Serial numbers are needed as a check against counterfeiting. You might validate the serial numbers against a master list and figure out if the bills in question were printed by the authorized currency issuer. However, the very act of validating a single number betrays your anonymity. If you do it electronically, it's pretty easy for the list owner to figure out the size of a transaction and where it is going down.

It would furthermore be possible to maintain a database of which serial numbered assets changed hands. Anonymity would be further compromised. It is like the Bitcoin or central bank digital currency problem.

Banks have cash machines that can quickly and accurately validate the authenticity of bills, usually in more than one currency. Whether they will weather this facility will remain after the widespread use of central bank digital currencies is a question that needs to be resolved. It is quite possible that widespread authentication of foreign currencies will not be possible. You need something that instead of being a voucher for value, like a banknote, has intrinsic value.

A voucher for value almost must be serial numbered. Without numbering, there is nothing to prevent the issuing authority from issuing endless quantities. But the serial numbering significantly compromises the on the anonymity of a transaction, an inherent weakness when dealing with currencies.

If you are given a gold coin, and you have the means of verifying that it is indeed made of gold, the problem disappears. The coin can be verified by its weight, its electrical properties, its magnetic properties, it's physical properties such as color, hardness, ductility or resonance when pinged.

Counterfeit gold coins are usually filled with tungsten, which is almost the same weight. Gold plating can get them past visual inspection. But they cannot pass the electrical tests of conductivity and resistance. They react differently in a magnetic field. And they would sound different when pinged or dropped.

Bank metals have retained their usage throughout the centuries because of the relative value property. Aluminum, copper and nickel have been used for smaller coins. More valuable coins have always been made of primarily gold and silver, but also at times platinum as well. At present gold is 90 times more valuable than silver, an ideal ratio. A one-ounce gold coin, about 20% smaller than a silver dollar, is currently worth $2500. The silver dollar, also one ounce, is worth about $30.

That means that a person could handle most common financial transactions anonymously with a combination of gold and silver coins, as long as the authenticity of the coins could be verified at a reasonable cost.

For small transactions it could be simply visual – look at the coin. If it is a gold coin it will probably come wrapped in a plastic package from the mint that stamped it. The same might be true of a silver coin.

If you want to go beyond visual verification, it would not be terribly hard to have a computer-attached device to weigh a coin and verify its electrical, magnetic and sound absorption/reflection properties. Suffice it to say that gold and silver coins, perhaps platinum as well would serve the purpose for most transactions.

The value of these coins relative to each other and to the CBDC fiat currency will vary day-to-day. The value of the coins involved will need to be computed at the time of the transaction in real time verification of price. A computer program can be written to do it quickly and anonymously.

There is also be the question of change. Assuming one was dealing in silver, where the smallest coin might be worth three or four dollars, the change would be enough to be worth keeping track of, but small enough that exchange-rates wouldn't matter. It could be paid via CBDC without compromising the anonymity of the whole transaction.

We can list the prices from the Internet for metals exchange and note that the units of the metal run from ounces for silver, gold, platinum and palladium up to metric tons for iron ore and steel. Along the way. We have pounds, kilograms, pounds and kilograms. The fact that only four metals are in the 1-ounce category pretty much tells the story. There are no other metals that would make sense as coinage. They simply don't exist in enough volume; they don't have a history of being used as coins and the values are not appropriate to being used as such.

Gold ingots are serially numbered by the issuers. If one were to submit the serial number for validation, it would blow our anonymity. But a passive system, whereby the manufacturers provided lists of all valid serial numbers with the flag of those for which duplicates had been reported – it would be a very good, but although less than 100% confirmation.

We could expect that issuers of silver and gold coins who were interested in selling their product could provide this if there were a market demand for. A government that was interested in seigniorage could do the same thing for their paper money. If Saudi rials were to be such a currency, they could provide lists of all valid serial numbers and flag those that are known to have been counterfeited.

Conclusion

Inflation and CBDCs will increase the utility of precious metals. They will be a better instrument for storing wealth than the alternatives of real estate and most corporate stocks. They allow anonymous transactions because their value is intrinsic. The major alternative at this writing, cryptocurrency, has significant advantages in the flexibility with which it can be employed. Offsetting these is the existential risk that the cryptography on which it depends will eventually be broken, and the shorter term risk posed by hackers at every link in the chain.

Precious metals’ track record is thousands of years long and there are compelling reasons why they will become even more attractive. Investors and entrepreneurs should be looking at ways enhance their utility for everyday transactions in the age of central bank digital currencies, ubiquitous government spying and rampant inflaction.

Solid and valuable insights!

To my mind the prospects of a future store of value are shares of well run companies that supply essentials. My Exxon shares have maintained their value but are subject to government whims. So far, such shares show growth is steady and inflation proof. I don't bother with speculation and hopes of a big payday from the shares supplying entertainment which can fail if economics get bad.

But we all need some well hidden metal coins or bricks of precious metals. I've tried physical stocks of beans/rice but they require monitoring and replacement cycles which gets harder as I age.

Given history of government revenue/outlay over a long time, 2% inflation has been OK and tolerable. That radically changed after 2008 as boomers retired; inflation/devaluation worldwide increased and won't likely return to normal (tolerable 2%) for a long time. As you note the demographics are awful. The disconnect between government policy and people's expectation is growing. As boomers pass away, their wealth transfers so spending might continue - then what?